Cleaning insurance is the coverage that protects homeowners and property managers from liability, property damage, and theft linked to professional cleaning services on their premises. Understanding the importance of cleaning insurance is not optional when you hire workers into your home or rental property. A single slip-and-fall accident, a broken heirloom, or a theft allegation can generate legal costs that far exceed the annual cost of a fully insured cleaning contract. Industry standards require cleaning companies to carry minimum $1M per occurrence in General Liability coverage, plus a Janitorial Bond and Workers’ Compensation. Knowing what those terms mean, and how to verify them, is the most practical thing you can do before a cleaner sets foot in your property.

Why does the importance of cleaning insurance matter to you?

Cleaning insurance is not just the cleaning company’s problem. When an uninsured cleaner injures themselves in your home, your homeowner’s policy may be the only coverage available. That means your premiums rise, your deductible applies, and your insurer may pursue you for negligence if you knowingly hired an uninsured worker.

The financial exposure is real. Legal defense costs are high even when theft allegations are unfounded, as Janitorial Bond claims show repeatedly. Property managers who oversee multiple units face compounded risk because every cleaning visit across every unit is a separate liability event. Requiring proof of insurance before work begins legally transfers that financial risk to the cleaning company’s insurer, not to you.

Cleaning service liability coverage also signals professionalism. A company that carries proper insurance has passed underwriting scrutiny, maintains safety standards, and has financial skin in the game. That vetting process filters out the lowest-quality operators before you ever open your door.

What types of coverage does cleaning insurance include?

Cleaning insurance commonly consists of a stack of up to ten separate coverage types. Each one addresses a different category of risk. The core four are General Liability, Janitorial Bond, Workers’ Compensation, and Commercial Auto.

Here is what each one covers and why it matters to you as a property owner:

- General Liability: Covers third-party bodily injury and property damage. If a cleaner breaks a window or a visitor trips over a mop bucket, General Liability pays. Most contracts require $1M per occurrence and $2M aggregate.

- Janitorial Bond: A financial guarantee that pays you directly if a cleaning employee steals from your property. This is not traditional insurance. It is a surety bond, and commercial contracts commonly require bond face values between $10,000 and $25,000.

- Workers’ Compensation: Covers the cleaner’s medical bills and lost wages if they are injured on your property. Workers’ Comp is legally required in nearly all states for cleaning businesses with employees. Without it, an injured worker can sue you directly.

- Commercial Auto: Covers damage caused by the cleaning company’s vehicles while traveling to and from your property.

- Pollution Liability: Covers chemical spills or fume damage from cleaning products. Standard Business Owners Policies exclude this risk entirely.

Annual costs for a small cleaning firm with 3–10 employees typically run $2,500–$6,500 per year. A solo cleaner pays $500–$1,500. Those numbers tell you that proper coverage is affordable. A company that skips it is cutting corners on your safety, not their overhead.

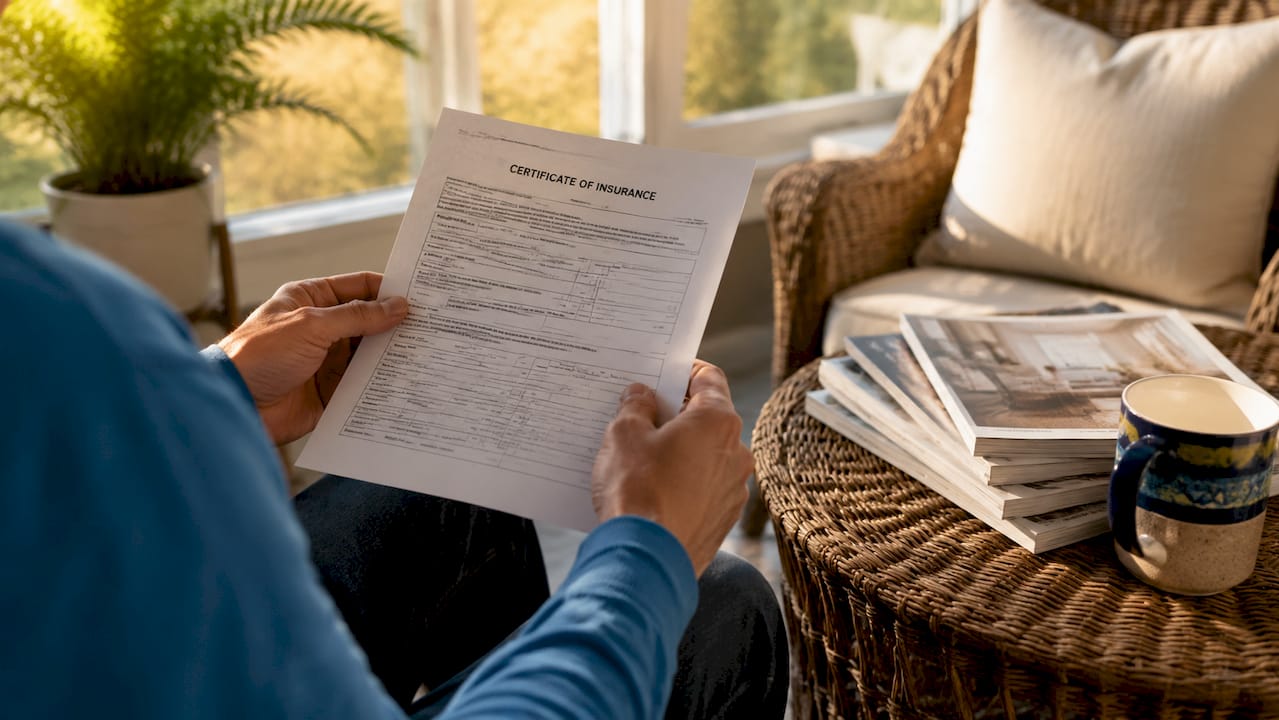

Pro Tip: Ask for a Certificate of Insurance before the first appointment, not after. Waiting until something goes wrong means the coverage question becomes a legal one.

Why do property managers require proof of cleaning insurance?

Requiring proof of insurance is the single most effective risk-transfer tool available to property managers. When you collect a valid Certificate of Insurance and confirm the required endorsements, you shift financial liability from your balance sheet to the cleaning company’s insurer.

The most common claims in residential and commercial cleaning fall into three categories:

- Slip-and-fall injuries: A cleaner slips on a wet floor they just mopped. Without Workers’ Comp, they can file a personal injury claim against you as the property owner.

- Property damage: Chemical damage to hardwood floors, a cracked countertop, or a broken fixture. General Liability covers these when the policy is properly structured.

- Theft allegations: A client reports missing jewelry or cash after a cleaning visit. Theft allegations are among the most common and costly claims in the cleaning industry. The Janitorial Bond pays the client directly and funds legal defense costs.

Property managers who oversee tenant-occupied units face an additional layer of complexity. Tenants can file claims against the property owner if a cleaning vendor causes damage or injury in their unit. Requiring the cleaning company to name you as an Additional Insured on their General Liability policy means their insurer defends you first.

Requesting proof of insurance is not just a vetting step. It is a legal mechanism that transfers financial risk to the cleaning company’s insurer in the event of accidents, damage, or theft. Property managers who skip this step absorb that risk personally.

Understanding cleaning scope requirements before signing a contract helps you align insurance demands with the actual work being performed.

What are the common coverage pitfalls to watch for?

The biggest mistake property owners make is treating a Certificate of Insurance as proof of adequate coverage. A COI is a summary document. It does not confirm endorsements, exclusions, or whether the policy limits match your contract requirements. A COI alone is insufficient to verify contractual protection.

The table below shows the most common coverage gaps and what fills them:

| Coverage gap | Why it matters | What fills it |

|---|---|---|

| Care, Custody and Control exclusion | GL policies exclude client property in the cleaner’s possession | Janitorial Bond |

| Employee theft | Standard Business Owners Policies exclude employee theft | Janitorial Bond |

| Chemical spills and fume damage | Pollution Liability excluded from standard GL | Specialized Pollution Liability endorsement |

| Specialty work (window cleaning, biohazard) | Height work and biohazard may be excluded or surcharged | Verify underwriting acceptance in writing |

| Under-insurance on high-value contracts | Policy limits below contract minimums leave gaps | Confirm limits match contract demands |

The Care, Custody and Control exclusion catches many property owners off guard. General Liability policies exclude property belonging to others that is in the cleaner’s possession. That means if a cleaner damages your furniture while moving it to clean underneath, standard GL may not pay. The Janitorial Bond covers this gap specifically.

Specialty cleaning creates additional underwriting complexity. Exterior window cleaning and biohazard work require verifying that the insurer has accepted those activities, not just that a policy exists. A policy that excludes height work is worthless for a window cleaning contract.

Pro Tip: Ask the cleaning company’s broker, not just the company, to confirm that all endorsements required by your contract are active on the policy. Brokers can provide written confirmation that a COI cannot.

Cleaners who reduce workplace risks through proper insurance and safety protocols represent a meaningfully lower liability exposure for property owners.

How can you verify that your cleaning service is properly covered?

Verification goes beyond collecting a single document. The process has five clear steps that any homeowner or property manager can follow.

- Request the Certificate of Insurance before work begins. Confirm it lists your name or company as an Additional Insured. Verify the policy effective dates cover the full contract period.

- Check the coverage limits against your contract. Most residential and commercial contracts require $1M/$2M General Liability. Higher-value properties or government contracts may require more.

- Confirm the Janitorial Bond is active. Ask for the bond number and face value. Commercial contracts commonly require bond values of $10,000–$25,000. Verify the bond covers all employees who will access your property.

- Request written confirmation of endorsements. Additional Insured, Waiver of Subrogation, and Primary & Noncontributory endorsements protect your interests. These must appear on the actual policy, not just the COI.

- Set a renewal reminder. Policies expire. A cleaning company that was properly insured in january may have a lapsed policy by july. Build a 30-day renewal check into your vendor management calendar.

Property managers overseeing multiple units benefit from working with insured cleaning services that provide updated documentation automatically at renewal. That removes the administrative burden and eliminates the risk of a coverage lapse going unnoticed. The cleaning insurance benefits of a properly vetted vendor extend beyond individual claims. They reduce your administrative exposure, protect tenant relationships, and keep your property management operation running without legal interruptions.

Key Takeaways

Cleaning insurance protects homeowners and property managers from liability, theft, and property damage by requiring cleaning companies to carry General Liability, a Janitorial Bond, and Workers’ Compensation before work begins.

| Point | Details |

|---|---|

| Core coverage stack | Require General Liability ($1M/$2M), Janitorial Bond, and Workers’ Comp at minimum. |

| COI is not enough | Always verify endorsements and policy limits directly with the insurer or broker. |

| Janitorial Bond fills the gap | General Liability excludes employee theft and client property in the cleaner’s possession. |

| Specialty work needs extra scrutiny | Window cleaning and biohazard work may be excluded from standard policies. |

| Ongoing verification matters | Check policy renewals annually and confirm endorsements remain active throughout the contract. |

Why I think most property owners underestimate this risk

I have seen the same pattern repeat itself across residential and commercial properties. A homeowner hires a cleaning company based on a referral and a good price. They never ask for insurance documentation. Six months later, a cleaner injures their back on the property, and the homeowner’s insurance carrier is suddenly involved in a workers’ compensation dispute that should never have touched them.

The uncomfortable truth is that most cleaning insurance oversights are not malicious. They are the result of assuming that a professional-looking company must be properly covered. That assumption is wrong often enough to matter. I have reviewed cleaning contracts where the vendor carried General Liability but no Janitorial Bond, meaning any theft allegation was entirely uninsured. The client had no idea.

The fix is not complicated. It is a 15-minute verification process done once before the contract starts and once at each renewal. The property owners who do this consistently never end up in those disputes. The ones who skip it are the ones calling their attorneys.

Proper insurance also changes the dynamic of the vendor relationship. A cleaning company that carries full coverage, maintains updated documentation, and responds quickly to insurance requests is demonstrating operational maturity. That is the kind of vendor worth keeping. Insured cleaning directly supports property value and tenant satisfaction over the long term.

— Wilker

Smartcleaningwa: insured cleaning for Seattle-area homeowners and property managers

Smartcleaningwa carries General Liability insurance and a Janitorial Bond on every residential and commercial cleaning engagement across the Greater Seattle Area, including Seattle, Kirkland, Bellevue, and Redmond. Proof of insurance is available before your first appointment.

Whether you need recurring house cleaning, a deep clean, move-in or move-out service, or Airbnb turnover cleaning, Smartcleaningwa meets the insurance and documentation standards that homeowners and property managers require. Every visit comes with real-time updates and reliable communication. Request your free cleaning estimate or review Smartcleaningwa’s residential cleaning services to confirm coverage details before booking.

FAQ

What does cleaning insurance typically cover?

Cleaning insurance covers third-party bodily injury, property damage, employee theft via a Janitorial Bond, and workplace injuries through Workers’ Compensation. Specialized policies also include Pollution Liability for chemical damage.

Is a Certificate of Insurance enough to verify coverage?

No. A Certificate of Insurance summarizes policy details but does not confirm endorsements or exclusions. Always verify Additional Insured status and coverage limits directly with the insurer or broker.

What is a Janitorial Bond and why does it matter?

A Janitorial Bond is a surety bond that pays property owners directly if a cleaning employee steals from their premises. General Liability policies exclude employee theft, making the bond a separate and necessary protection.

Do homeowners need to require Workers’ Compensation from cleaners?

Yes. Workers’ Compensation is legally required in nearly all states for cleaning businesses with employees. Without it, an injured cleaner can file a personal injury claim against the property owner directly.

What endorsements should property managers request on a cleaning policy?

Property managers should request Additional Insured, Waiver of Subrogation, and Primary & Noncontributory endorsements. These must appear on the actual policy, not just the Certificate of Insurance, to provide contractual protection.

Recommended

- Smart Cleaning Service™ House Cleaning Seattle Kirkland Bellevue Redmond

- Cleaning Scope of Work: What Property Managers Must Know

- Smart Cleaning Service™ House Cleaning Seattle Kirkland Bellevue Redmond

- Why Automate Property Cleaning: A Manager’s Guide